Algorithmic Trading

In algorithmic trading, the trading process is automated according to a set of pre-programmed rules and strategies that account for variables such as time, price, and volume. This enables investors to trade quickly, accurately and at reduced costs.

The computerization of the order flow that began in the early 1970s paved the way for modern algorithmic trading practices. Algorithmic trading relies on computer programs with predefined criteria (often proprietary algorithms) to automatically execute trades. For example, algorithmic trading is often applied by institutional investors whose large orders would cause excessive price impact if executed entirely at once. To avoid price impact to the market, large order execution algorithms are used to slice the single large order into many smaller orders that are sent to the market over time (SEC, 2014, pg. 5).

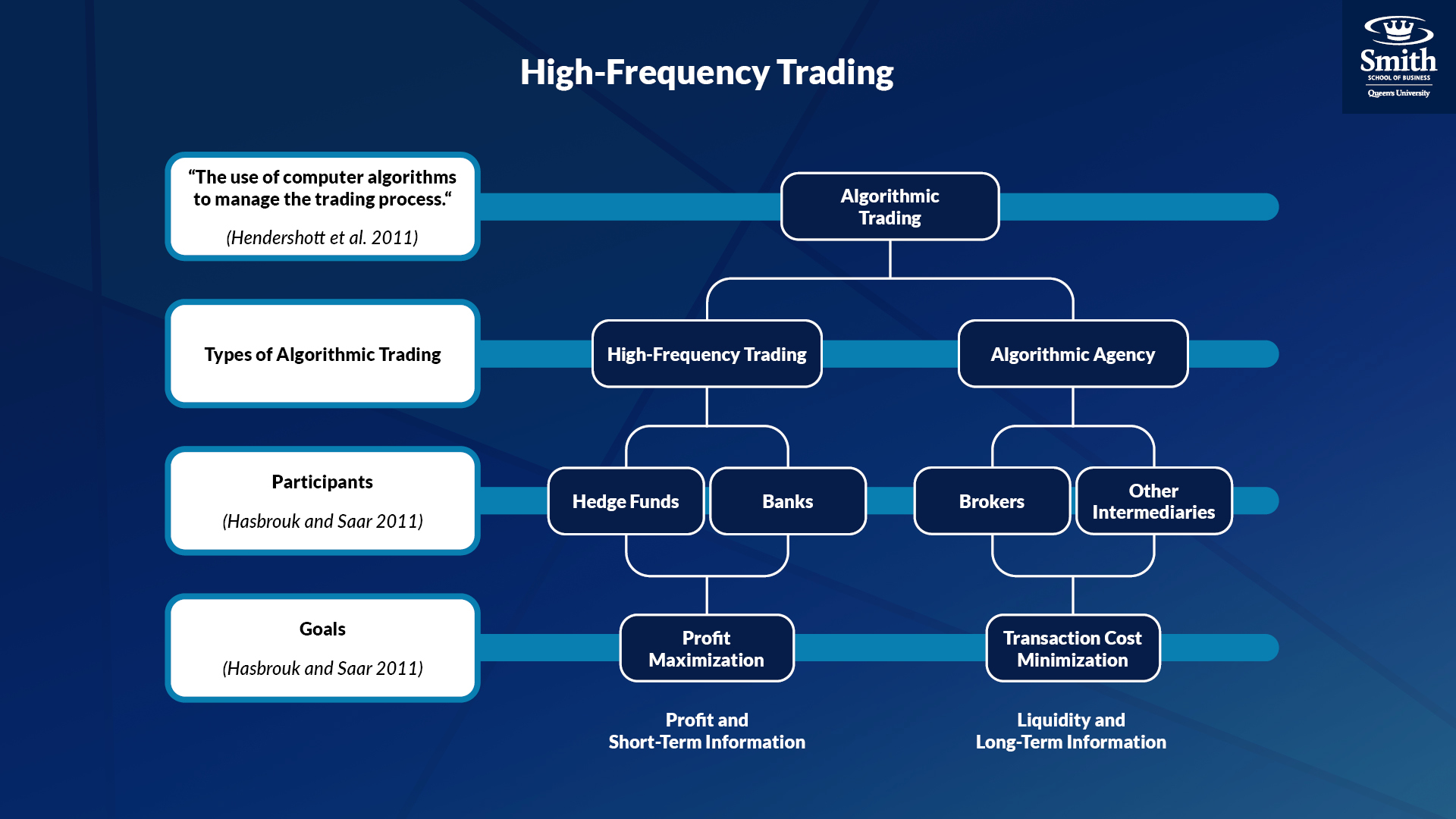

Algorithmic trading encompasses a range of trading activities, one of which is high-frequency trading. Review the diagram below which depicts this relationship.

ReferencesU.S. Securities and Exchange Commission (SEC). (2014). Equity Market Structure Literature - Review Part II: High Frequency Trading. Retrieved on August 6, 2020 from https://www.sec.gov/marketstructure/research/hft_lit_review_march_2014.pdf